Case Outline: Mr. Smith is 57 years old, married, owns a primary residence and has a net worth of over 3 million, not including his IRA accounts. Prior to contacting us, Mr. Smith and his wife had been researching the possibility of purchasing a second home in Panama. After completing our compatibility form and consulting with us, Mr. Smith-working through a Panamanian lawyer, entered into a purchase and sale agreement with a Panamanian building corporation to purchase of of their pre-construction homes. Several deposit commitments are scheduled during the construction phase, which are to be paid for by non IRA monies. Since Mr. Smith did not have available liquid assets for these deposits he obtained a home equity line of credit against his primary residence for $100,000. Upon construction completion, a mortgage arranged by us through Eldorado bank in Panama in coordination with Chase Manhattan Bank in the US, would finance the balance of the purchase price of approximately $400,000. We assisted Mr. Smith in placing approximately $390,000 of his IRA in a SAFE HARBOR®-Directed IRA™ (SHIRA™) account-the structural foundation to his IRA real estate plan. This SAFE HARBOR®-Directed IRA™ (SHIRA™) account, guaranteed to earn a minimum of 3% with a potential of 4%-5% as a ten-year average and insures against loss of principal value due to investment exposure during the life time of the contract. We then structured Mr. Smith’s SHIRA™ account to provide an income stream to be used initially to pay interest and principal on the HELOC and then eventually on the home mortgage. Any tax liability generated by this income stream was calculated to be offset by allowable tax deductions. Ultimately, Mr. Smith and his wife plan to sell their home in the western United States and relocate full time to Panama. At that time, they will be able to keep any capital gain in such a way as to supplement their retirement income. Mr. Smith’s IRA will continue to make the mortgage payments on their home in Panama for a minimum of 18 years, with a potential of up to 27 years depending upon the interest he receives in his SHIRA™ account.

Summary: The IRA Real Estate plan enabled Mr. & Mrs. Smith to purchase their eventual retirement home immediately, prior to selling their existing primary residence. By structuring Mr. Smiths’s IRA to support the purchase of the home in Panama the Smiths are able to use their home in Panama for vacations thereby benefiting from both homes until they are ready to relocate full time without effecting their current income stream. When they are ready to retire and transfer residency to Panama, the tax free portion of proceeds from their primary residence will not only replace, but exceed by far the value of the IRA used to purchase their retirement home. Additionally, there are estate planning benefits to this IRA Real Estate plan that are not covered in this brief synopsis.

STRATEGICALLY OPTIMIZE YOUR IRA FUNDS FOR REAL ESTATE THAT YOU CAN ACTUALLY USE AND CREATE INCOME FROM.

We help people multiply their IRA funds by directing them to purchase real estate that they can personally use or create an additional income from, so that they can have more flexibility in their retirement, as well as create certainty and security for their families and leave a larger and more impactful legacy.

One last thing.

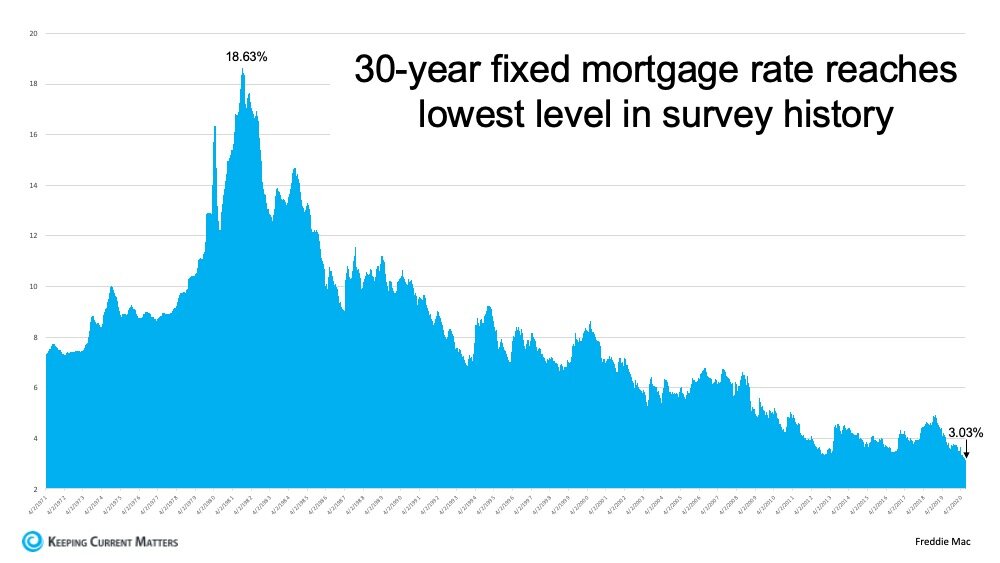

With the extreme volatility, the market has been experiencing the last few months, not a single client of ours has incurred a loss of value to their SHIRA™.

In fact, according to a report from Zillow, real estate increased in value an average 5.46% in 2019 nationwide, along with the asset protection of their SHIRA™, possible rental income, tax benefits, and the intrinsic value of occupancy of the property, our clients enjoy confidence, peace of mind and growth with their SAFE HARBOR®-Directed IRA™ (SHIRA™) real estate investment and its bottom line.